Designing financial inclusion for farmers who shared one phone between three people and had never used a bank.

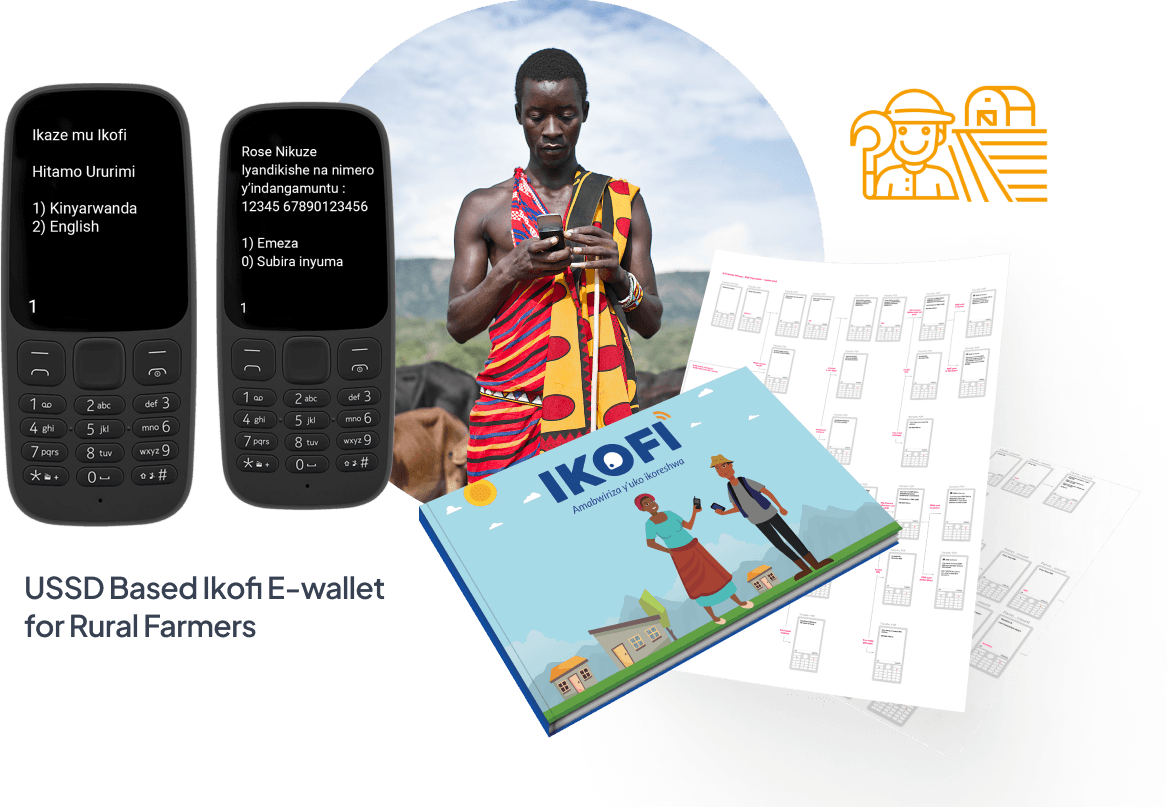

Led design for Ikofi a dual-product USSD wallet and Android app that brought 260,000+ rural Rwandan farmers into the formal financial system.

Client

Bank of Kigali, Rwanda

in collaboration with McKinsey & Company

Engagement

8 months on-site · Fractal Ink

Platform Impact

260,000+ farmers and agro-dealers onboarded · 300+ coffee washing stations · launched 2019

Role

Lead UI Designer

USSD journey flows, Android app, visual direction, marketing collaterals

Team

The Problem

Rwanda's rural farmers were economically active but financially invisible.

The farmers growing Rwanda's coffee and agricultural crops were participating in a functioning economic system buying seeds and fertilizer from agro-dealers, selling harvests to washing stations, earning income through cooperatives. Money moved through this ecosystem constantly. Almost none of it moved through a bank.

The reasons were practical, not just behavioral. Branch banking required travel that subsistence farmers couldn't afford. Most transactions were cash-based by necessity. Digital banking required a smartphone and literacy that most rural farmers didn't have. And in many farming households, one mobile phone was shared between two or three people an economic and logistical reality that standard financial product design had never accounted for.

Bank of Kigali wanted to change this. The goal was genuine financial inclusion: not a product built for urban customers and offered to rural ones, but a financial system designed from the ground up for people who had never interacted with formal banking before.

The design challenge wasn't building a banking app. It was designing a financial system that could operate within the actual constraints of rural Rwandan agricultural life shared phones, low literacy, Kinyarwanda as the primary language, and trust networks built around cooperatives, not institutions.

Hard Contraints

• USSD-only for farmers: text-based, menu-driven, works on any basic phone, no internet required the only viable channel for users who may not own a smartphone

• Shared phone reality: 2–3 farmers per phone meant the experience had to be session-based, secure, and completable quickly between handoffs

• Low literacy rate: financial terminology, instruction text, and menu options had to be understandable to users with limited reading ability

• Kinyarwanda as the primary language: designed and tested in both English and Kinyarwanda translation wasn't an afterthought, it shaped the interaction logic

• Dual user base with different needs: farmers needed USSD simplicity; agro-dealers managing inventory and payments needed a full Android app

• Trust mapped to cooperatives, not banks: the product had to leverage existing cooperative trust structures, not replace them

My Role

I worked closely alongside the Principal UX Designer supporting empathy mapping, user testing fieldwork, and USSD journey flow creation while simultaneously leading the design direction for the full Ikofi product: the Android mobile app for agro-dealers, the visual identity, and all marketing and print collaterals. The engagement required operating across two registers at once: the radical constraint of USSD design for low-literacy farmers, and the visual design challenge of creating a product identity that was culturally resonant for rural Rwanda.

The Reframe

The brief was to build a mobile wallet. The real problem was designing for people who had never been the intended user of any digital product.

"Standard fintech design assumes a smartphone, assumes literacy, assumes the user is the product's primary audience. Ikofi's users were none of those things. Every assumption had to go."

The brief framed Ikofi as a mobile wallet for rural farmers implying a product in the established fintech tradition, adapted for a different market. Field research in Rwanda showed how far that framing was from the reality.

Farmers shared phones. Not as an edge case as a normal operational reality. Two or three farmers might pass a single handset between them to complete a transaction. A session had to be completable before the phone was handed over. Multi-step flows, screen-by-screen onboarding, complex menu hierarchies all of the UX patterns that fintech products relied on were unusable in this context.

Low literacy wasn't a minority condition it was the baseline. Menu text, transaction confirmations, error messages, and instructions all had to work for users who might read slowly or not at all. Icon systems, simplified language, and Kinyarwanda-first copy were not accessibility accommodations they were primary design requirements.

And trust didn't flow through institutions. Rural Rwandan farmers trusted their cooperative leaders, their agro-dealers, their community networks. A bank brand meant little without connection to those existing trust structures. The product had to integrate into the cooperative ecosystem not compete with it.

That reframe changed everything. Ikofi wasn't a banking app for underserved users. It was a financial layer designed to fit within the existing social and economic structures of rural agricultural life. The design had to disappear into those structures, not ask users to adapt to it.

Why This Was Hard

USSD is the most constrained design medium in digital product design. Every character matters.

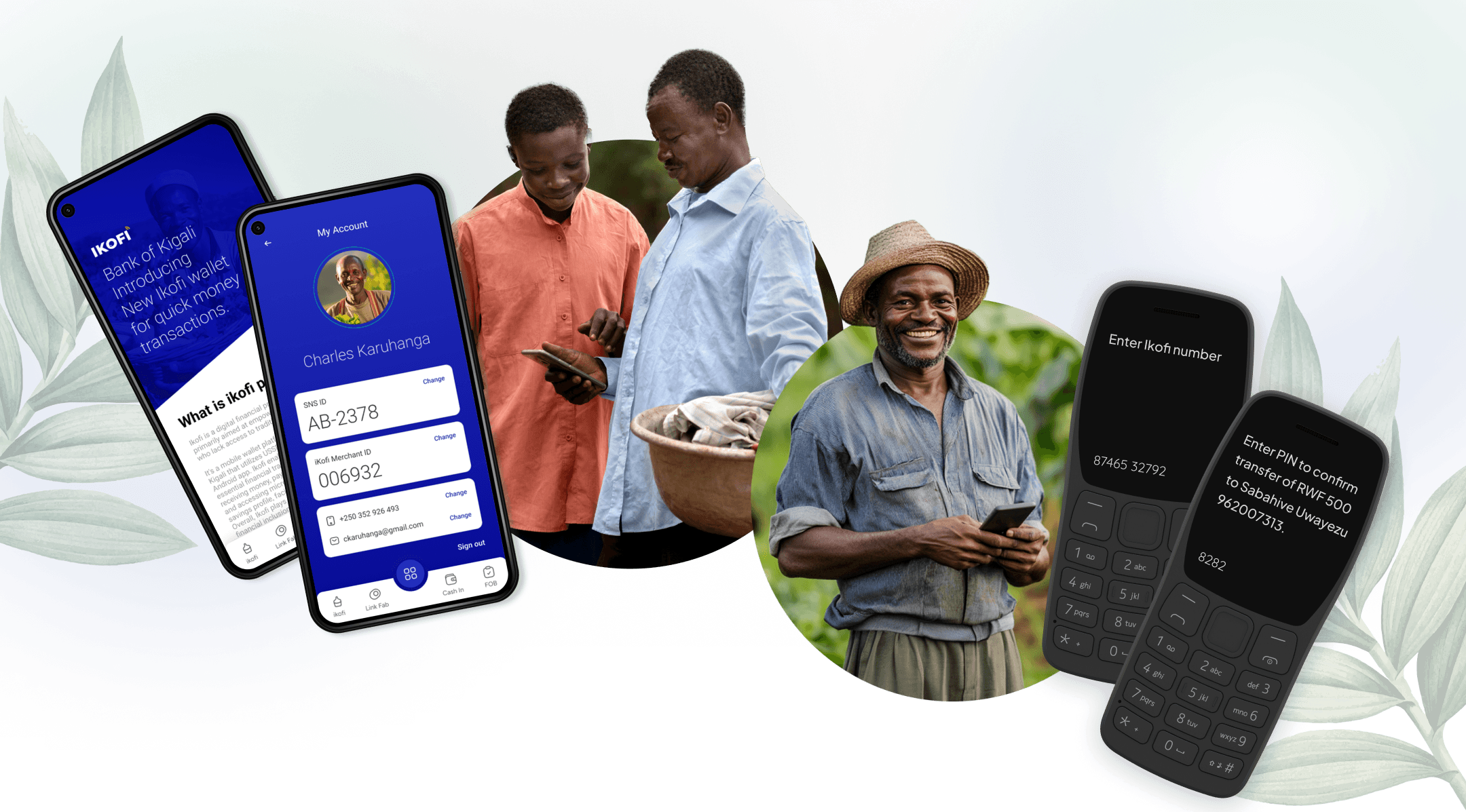

USSD (Unstructured Supplementary Service Data) is text-only, menu-driven, and stateless. No images. No color. No persistent sessions. Works on any mobile phone without internet. It is the most constrained interaction design medium that exists at scale and it was the only viable channel for a population of farmers with basic handsets and limited data access.

Contraint 1

USSD character limits and menu depth

What it required : Financial journeys had to be compressed into numbered menu options and short text strings. Every word of copy had to be essential. Menu hierarchy had to be flat enough to navigate without getting lost.

Contraint 2

Shared phone sessions between farmers

Transactions had to be completable in a single, short session. No saved progress. No returning to a half-completed flow. Security PINs protected individual accounts on a shared device.

Contraint 3

Low literacy in two languages

All text — menu options, confirmation messages, error states — designed for users who might read slowly or rely on pattern recognition. Kinyarwanda copy required working closely with translators and testing directly with farmers.

Contraint 4

Dual product complexity

USSD for farmers and Android app for agro-dealers had to work as an integrated system — transactions initiated on one platform completing on the other, without either user experiencing the complexity of the integration.

Contraint 5

Trust through cooperative structures

The onboarding pathway for farmers ran through cooperative leaders, not through app stores or bank branches. The design had to work within that distribution model, not assume direct user acquisition.

Process & Decisions

Three decisions that defined Ikofi.

Decision 1 : USSD for farmers, android for Agro-dealers

The initial product direction was a single mobile wallet solution. Field research and ecosystem mapping revealed that the two primary user groups farmers and agro-dealers had fundamentally different device access, literacy levels, and workflow requirements that a single product couldn't serve.

Farmers: basic handsets, limited literacy, shared phones, need for the simplest possible transaction flow. USSD was the only viable channel it required no smartphone, no app download, no internet connection, and worked on every mobile network in Rwanda.

Agro-dealers: managing inventory, processing multiple transactions per day, coordinating with cooperative networks and washing stations. They needed a full app with account management, transaction history, inventory tracking, and the ability to accept payments from farmers' USSD wallets.

I contributed to the decision to design both products simultaneously as an integrated system rather than a single product with two modes. The USSD wallet and the Android app had to feel coherent to the ecosystem even though they were built for entirely different devices and interaction models. This decision defined the scope and shaped every subsequent design choice.

"Two products, one system. Farmers pay on USSD. Agro-dealers receive on Android. The transaction completes seamlessly across the channel gap."

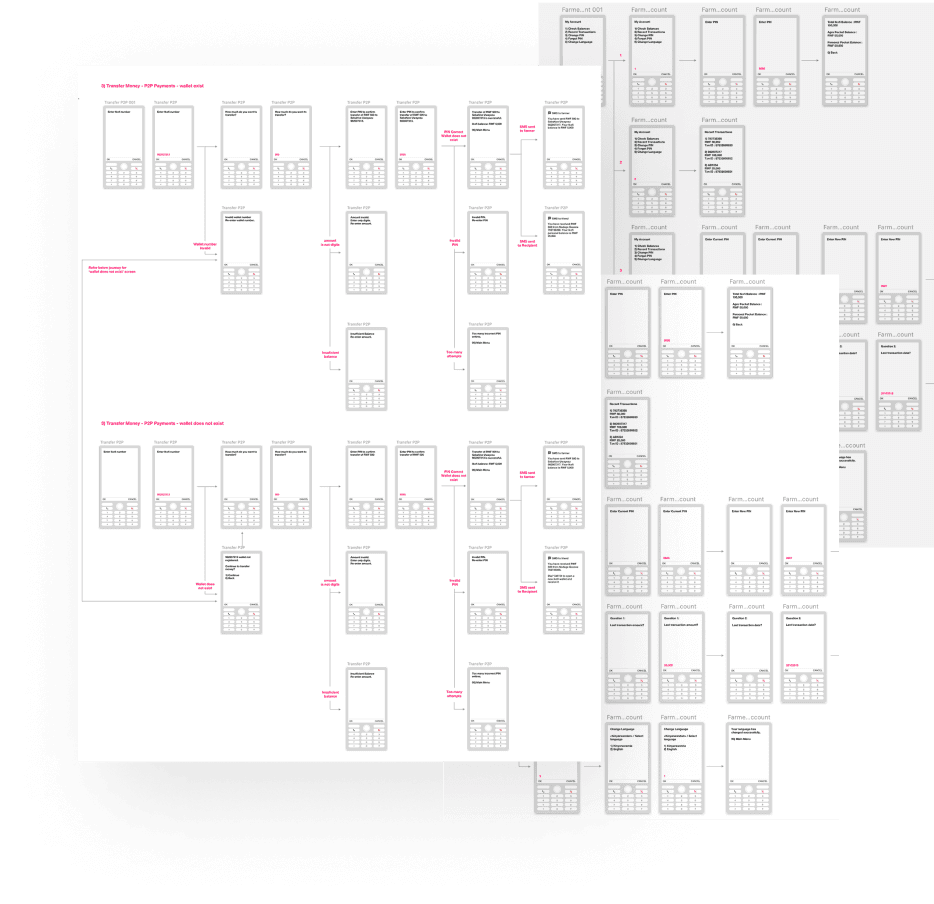

Decision 2 : USSD Journey architecture mapped to numbered steps

Designing USSD flows required a completely different approach from any other product design in this portfolio. There is no screen, no visual hierarchy, no color, no iconography. There is text short, numbered menu options and the user's ability to remember where they are in a sequence they cannot see in full.

The hardest USSD design challenge was mapping financial journeys balance check, money transfer, payment for agricultural inputs, loan application into menu trees that a low-literacy user could navigate correctly without a guide. This required working closely with the UX Designer to define the exact sequence of numbered options, the precise wording of each menu item in both English and Kinyarwanda, and the confirmation and error states that would prevent incorrect transactions.

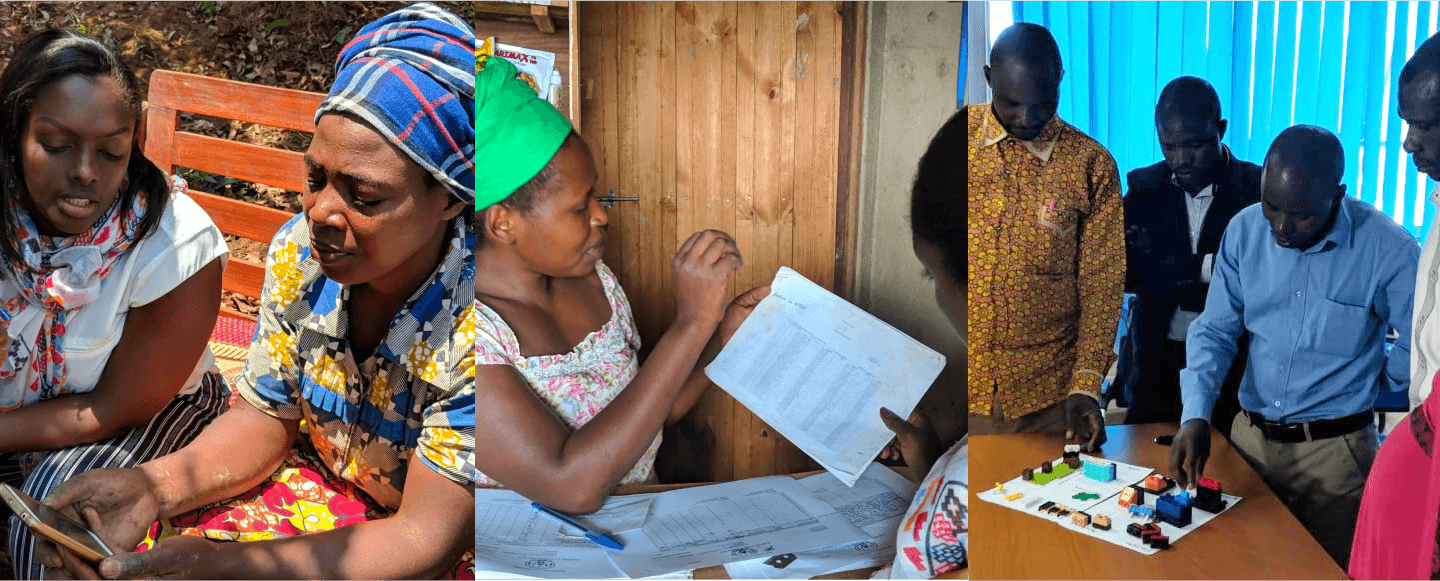

Usability testing with farmers conducted in Kinyarwanda with translation support was the validation mechanism. Users navigating the USSD prototype in Kinyarwanda revealed specific points where menu wording was ambiguous, where the sequence felt counterintuitive, or where a transaction confirmation didn't give enough information to verify before committing. Each testing round refined the journey flows directly.

The discipline of USSD design: every additional menu level is a navigation burden. Every extra word in a menu option is a literacy barrier. Every confirmation step that doesn't add genuine safety is friction without value. The final USSD journeys were as short as the transactions allowed no step included unless it served a clear user or safety purpose.

"Numbered menus, short text, Kinyarwanda-first. Every step validated with farmers in the field. No navigation step included unless essential."

Decision 3 : Visual identity rooted in Rwandan agricultural culture

The Android app and all Ikofi marketing materials required a visual identity that communicated trust, accessibility, and cultural relevance to rural Rwandan farmers and agro-dealers an audience that had never been the primary target of a digital financial product.

The moodboard exploration produced two directions: a modern international aesthetic using negative space and subdued tones, and a vibrant pattern-based direction drawing from Rwandan cultural visual language bold colors, repetition, and human-centric imagery. The team chose the second direction not because it was more beautiful, but because it was more recognizable. Farmers and agro-dealers encountering Ikofi for the first time needed to feel that the product was made for them, not adapted from somewhere else.

The visual language for the Android app used this direction: vibrant color, culturally resonant imagery, and simplified iconography designed to communicate function without relying on text. For users whose primary language was Kinyarwanda and whose literacy was limited, icons carried more navigational weight than they do in any other product in this portfolio. Every icon had to be unambiguous in the context of agricultural financial transactions.

The marketing and print collaterals extended the same visual language into physical materials distributed through cooperative networks and agro-dealers posters, instruction cards, and onboarding materials that farmers would encounter before they ever opened the app or dialed the USSD code.

"Visual identity chosen for recognition, not just aesthetics. Rural Rwandan farmers needed to feel the product was made for them not adapted from a global fintech template."

The Solution

A dual-product financial system designed for the actual constraints of rural Rwandan agricultural life.

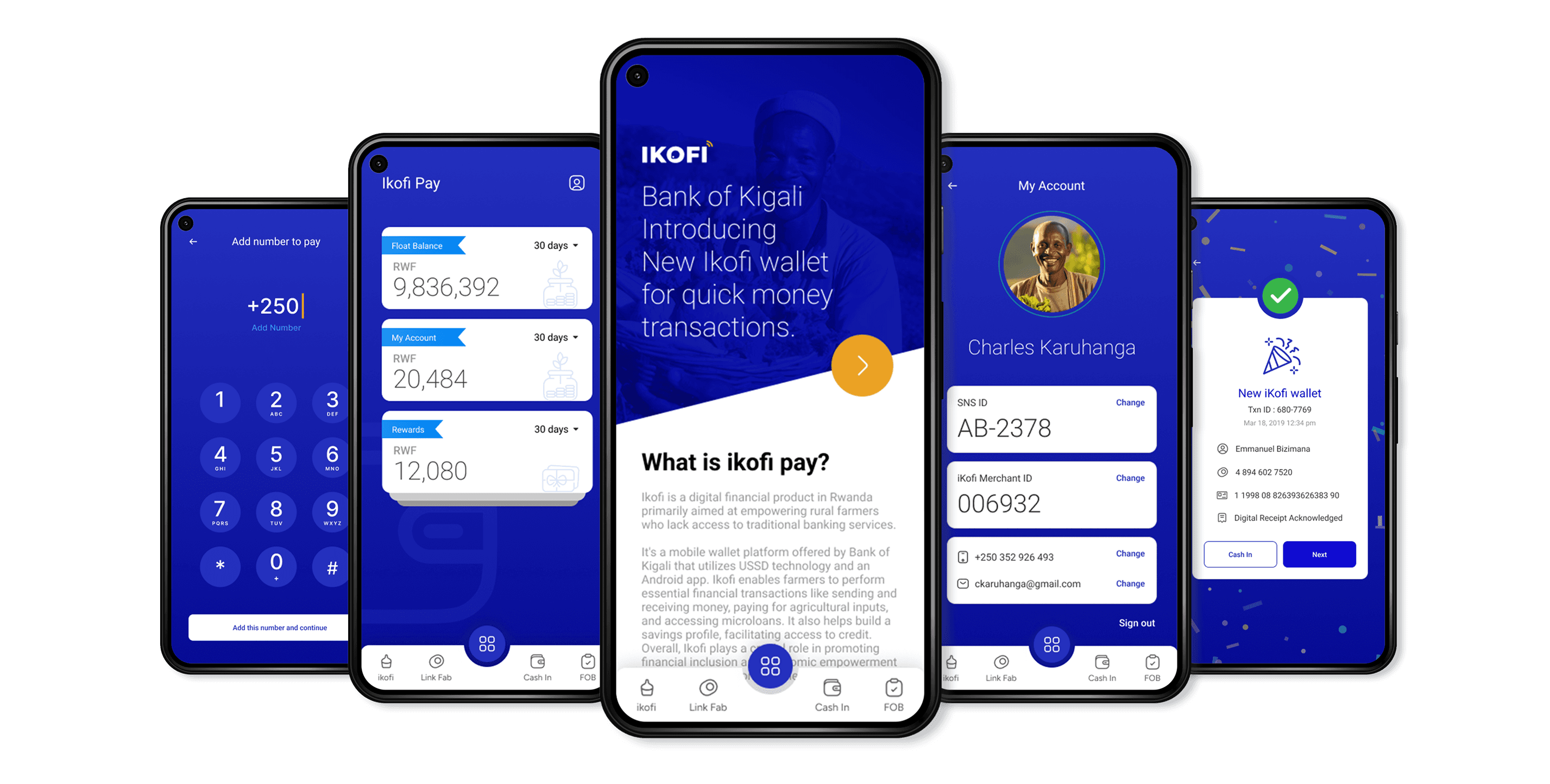

USSD Wallet for Farmers

Text-based financial access requiring no smartphone, no internet, no app download. Balance check, money transfer, payment for agricultural inputs, loan access all accessible through numbered menu navigation in English and Kinyarwanda. Session-based with PIN security for shared-phone use. Designed for users navigating financial transactions for the first time, on a device they may share with two other people.

"Every menu option in Kinyarwanda. Every journey validated with farmers in the field. USSD because it was the only channel that worked for every farmer, on every phone, in every location."

Android app for Agro-dealers

Full mobile app for agro-dealers managing agricultural input sales, inventory, and payments across multiple farmer customers. Accept payments from farmers' USSD wallets. Transaction history and account management. Cooperative network integration. Designed for users with more device familiarity and more complex operational needs than the farmers they serve.

"The agro-dealer receives on Android what the farmer sends on USSD. Two different products, one seamless transaction."

Visual Identity and Marketing Collaterals

Brand identity, Android app visual language, and print marketing materials all built on the vibrant, pattern-based Rwandan cultural aesthetic. Distributed through cooperative networks and agro-dealers as physical onboarding materials before farmers ever opened the digital product. The physical touchpoint was the first introduction to Ikofi for most farmers.

Cooperative Integration

Ikofi was designed to distribute through existing cooperative trust structures not to replace them. Cooperative leaders served as onboarding intermediaries, introducing farmers to the USSD wallet within trusted community networks. The product's adoption pathway was designed around how rural Rwandan agricultural communities actually worked.

Impact

The following outcomes are drawn from public reporting on the Ikofi platform following its 2019 launch — the product designed during this 2018 engagement.

260,000+ rural farmers and agro-dealers onboarded onto the Ikofi platform

300+ coffee washing stations integrated into the cashless payment system

Farmers connected to formal banking services Bank of Kigali uses transaction data for loan access

NFC-enabled cashless transactions at washing stations via key fobs

Partnerships with RWACOF and others: tens of thousands of farmers trained in digital financial literacy

Platform continues to expand 400,000+ Rwanda coffee farmers targeted for cashless adoption

Ikofi became the platform that brought over a quarter of a million rural Rwandan farmers into the formal financial system not by asking them to change how they lived and worked, but by designing a product that fit within those lives. USSD because that's the channel that worked. Kinyarwanda because that's the language that worked. Cooperative distribution because that's the trust network that worked.

"Ikofi's launch increased financial inclusion and financial literacy among rural farmers. It continues to evolve, driving economic development and improving lives in Rwanda."

The design decision to build two separate products USSD for farmers, Android for agro-dealers was validated at scale: the system worked because it met each user where they were, not where a single product assumed they would be.

Reflection

What this project taught me about inclusive design

Inclusive design is not adding accessibility features to an existing product. It is designing from the constraints of the most excluded user first and working outward from there. USSD design forced a discipline that every product I've designed since has benefited from: if you can design a financial journey in plain text with numbered menus, you can design it for anyone. The constraints didn't limit the product they defined it.

What field testing in Kinyarwanda taught me

No research conducted at a desk prepares you for watching a farmer navigate your USSD prototype for the first time, in their first language, with their actual phone. The points where users hesitated, re-read, or chose the wrong menu option were not visible from the journey documentation they were only visible in the room. Remote usability testing would have missed them all. The fieldwork was the design work.

What the shared phone reality changed

Designing for shared phone use required questioning assumptions about session persistence, saved progress, and user identity that I'd never had to question before. When 2–3 people use the same device, 'the user' isn't a stable concept. Security, session management, and transaction confirmation all had to be designed with that instability as the starting point. It's a constraint I now think about whenever a product assumes persistent individual device ownership.

What I'd do differently

Start the Kinyarwanda copy design earlier and treat it as a design input, not a translation output. We worked closely with translators throughout, but the Kinyarwanda version of some USSD menus revealed structural issues in the journey logic that the English version had hidden because Kinyarwanda phrasing for financial concepts sometimes required more words than the English equivalent, which affected menu depth and readability. Designing in Kinyarwanda first and adapting to English would have surfaced those issues earlier.

Why this project matters in the portfolio

Every other case study in this portfolio is a sophisticated product for sophisticated users government employees, corporate banking RMs, MSME owners, urban consumers. Ikofi is the opposite: the simplest possible product for the most constrained users in the most resource-limited context. That contrast is intentional. It shows that the design thinking that produces a GovGPT trust architecture or a Riyad Bank loan journey applies equally to a USSD wallet for a farmer who shares a phone and reads slowly. The principles are the same. The applications are as different as they can be.